Last-Minute Tax Saving Moves Before April 1 2026: Section 80C Investments Checklist

The financial year is ending on March 31, 2026, and if you haven’t locked in your Section 80C investment checklist yet, there’s still time—but only if you act now. With just weeks left, thousands of Indian salaried employees, freelancers, and business owners are scrambling to maximize tax deductions under Section 80C of the Income Tax Act. The challenge? Not all Section 80C investments can be completed at the last minute, and missing the deadline could mean losing tax benefits worth ₹1.5 lakhs or more. This guide breaks down exactly which Section 80C investments you can still make, which documents you’ll need, and what happens if you miss the cutoff.

What Is Section 80C and Why Is It Critical for Your Tax Savings?

Section 80C of the Income Tax Act allows Indian taxpayers to claim deductions up to ₹1.5 lakhs per financial year on specific investments and expenses. This deduction directly reduces your taxable income, which means lower taxes owed and potentially bigger refunds.

For example, if your taxable income is ₹8 lakhs and you invest ₹1.5 lakhs in Section 80C instruments, your new taxable income drops to ₹6.5 lakhs. Depending on your income slab, this could save you anywhere from ₹30,000 to ₹60,000 in taxes annually.

According to SEBI guidelines and RBI documentation, Section 80C investments are not just tax-saving tools—they’re also wealth-building instruments. Popular financial educators like Ankur Warikoo and CA Rachana Ranade frequently emphasize that combining tax benefits with actual asset creation (through Life Insurance, PPF, or ELSS) is the smarter approach than simply looking for deductions.

Section 80C Investment Checklist: What You Can Still Complete Before March 31, 2026

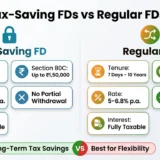

1. Public Provident Fund (PPF) – Can Be Done Until March 31

Deadline: March 31, 2026 (hard cutoff)

Investment Limit: ₹1.5 lakhs per financial year (minimum ₹500)

How to Complete:

- Visit any nationalized bank (SBI, HDFC Bank, ICICI Bank) or post office

- Fill PPF Form A (for new accounts) or Form B (for existing accounts)

- Submit KYC documents (Aadhaar, PAN, passport, driving license—any one)

- Deposit cash or cheque

- Get acknowledgment slip with PPF account number

Tax Benefit: ₹1.5 lakhs deduction + zero tax on interest earned (Section 80C + 10(13))

Why PPF Works: Even at the last minute, PPF deposits can be made on March 31, 2026. Many banks stay open late or offer online PPF facilities. The interest rate for Q4 FY 2025-26 is typically 7-7.5% p.a. (rates are reviewed quarterly).

2. Life Insurance Premiums – Deadline: March 31

Deadline: March 31, 2026 (premium must be paid, not just proposed)

Deduction Limit: Varies by policy, but typically limited within ₹1.5 lakhs total Section 80C

How to Complete:

- Contact your insurance provider (HDFC Life, ICICI Prudential, LIC India) online or offline

- Pay annual premium via net banking, UPI, or cheque

- Ensure payment clears before March 31

- Request premium receipt dated on or before March 31

Documents Needed: Policy number, premium receipt with date, proof of payment (bank statement/cheque)

Critical Note: If your premium due date falls on April 2, paying early (before March 31) will count toward the current FY. However, if you pay after April 1, it will be deductible in FY 2026-27.

3. Equity-Linked Savings Scheme (ELSS) Mutual Funds – Can Still Be Bought

Deadline: March 31, 2026 (order must be placed and settled before EOD)

Minimum Investment: ₹500 (via SIPs or lump sum)

How to Complete:

- Open account on Groww, Zerodha (Coin), ET Money, or INDmoney

- Complete KYC (Aadhaar, PAN, bank details)

- Place lump-sum or SIP order in ELSS schemes

- Ensure fund house confirms order settlement on March 31

Best ELSS Options (As of 2026): Axis ELSS Tax Saver, HDFC Tax Saver, Motilal Oswal ELSS, Mirae Asset ELSS. Returns vary; historically 12-15% annualized over long periods.

Tax + Wealth Combo: ELSS offers both ₹1.5 lakhs deduction AND potential capital appreciation. The 3-year lock-in period ensures disciplined investing.

4. Employee Provident Fund (EPF) Contributions – Already Ongoing

Deadline: Continuous (employer deducts monthly)

Annual Contribution Limit: Up to ₹2.5 lakhs per year (but typically capped at ₹1.5 lakhs for Section 80C deduction)

Action Required: No special action needed for employed individuals—your employer already deducts EPF. However, you can make voluntary contributions via your employer’s HR portal if FY contribution is still below ₹1.5 lakhs.

5. National Savings Certificate (NSC) – Deadline: March 31

Deadline: March 31, 2026

Investment Limit: No upper limit per se (within reason), but deduction capped at ₹1.5 lakhs Section 80C

How to Complete:

- Visit SBI, HDFC Bank, ICICI Bank, or post office

- Fill NSC application form

- Submit KYC documents

- Pay amount in cash or cheque

Current Interest Rate (FY 2025-26): Approximately 7.7% p.a., compounded annually

Lock-In: 5-year maturity (can be extended further)

6. Home Loan Principal Repayment – Already Being Paid

Deadline: Not applicable (deduction claimed in the year payment is made)

Deduction Limit: Principal amount actually repaid during FY (within Section 80C cap)

Action Required: No urgent action needed—your bank statements will show principal repayment. However, if you’re making an extra principal payment before March 31, ensure it’s processed by EOD March 31.

What You CANNOT Complete After March 31: Important Exclusions

1. Investment Proposals Without Payment

SEBI guidelines are clear: A proposal, application, or promise to invest does not count. The payment must be completed and cleared before March 31, 2026. If you submit a proposal on March 30 but payment clears on April 5, it won’t be deductible in FY 2025-26.

2. Tuition Fees Paid After March 31

Education fees under Section 80C must be paid before March 31 to count toward that financial year. A fee due in April will be deductible in FY 2026-27, not 2025-26.

3. Stamp Duty and Registration for Property Purchases

If you’re buying property, stamp duty and registration costs are deductible under Section 80C—but only when paid. If payment is delayed to April, the deduction shifts to next year.

Step-by-Step Action Plan for Last-Minute Tax Savings (By Priority)

Week 1 (Before March 24)

- Calculate Remaining 80C Limit: Subtract all investments made year-to-date from ₹1.5 lakhs. Use tax software like ClearTax, ET Money, or your CA’s spreadsheet.

- Check Bank Balance: Ensure you have sufficient liquid funds to invest. PPF, NSC, and ELSS require immediate payment.

- List Pending Payments: Home loan principal, insurance premiums, education fees—check which are still due before March 31.

Week 2 (March 25-30)

- Prioritize High-Liquidity Instruments: ELSS (via Groww/Zerodha—instant online) and PPF (available at banks until 5 PM on March 31) first.

- Complete KYC if Pending: If using Groww or ET Money for the first time, finalize KYC by March 28 to allow 2-3 days for approval.

- Make Policy Payments: Call your insurance agent or log into HDFC Life / ICICI Prudential app and ensure premium clears before EOD March 31.

- Submit Home Loan Principal Pre-Payment: Log into SBI/HDFC/ICICI net banking and schedule extra principal payment for March 30 or 31.

Week 3 (March 31)

- Final Deposit Day: PPF and NSC deposits at post offices and banks close at 3-4 PM, so deposit early morning.

- ELSS Lump-Sum Order: Place final order on Zerodha Coin or Groww before 3 PM to ensure settlement today.

- Collect Receipts: Get acknowledgment slips, premium receipts, and payment confirmations. Take photos or PDFs for your records.

Documents You’ll Need for ITR Filing (April Onwards)

Don’t lose these papers once you’ve invested:

- PPF: PPF passbook or statement, deposit receipts with dates

- Life Insurance: Premium receipt, policy document (first page), proof of payment

- ELSS: Folio statement from mutual fund or app, transaction confirmations

- NSC: NSC certificate or statement, acknowledgment slip

- EPF: Annual EPF statement (downloaded from Unified Portal)

- Home Loan: Bank statement showing principal repayment, loan account statement

- Education Fees: Receipts from school/college, fee payment confirmation

Keep these in a dedicated folder (digital or physical) for 5-7 years. The Income Tax Department can ask for proof during assessment.

Common Mistakes That Cost You Deductions

1. Paying with a Cheque That Clears After March 31

Avoid this. Use NEFT/RTGS or cash for same-day settlement. If using cheque, ensure it’s deposited and cleared by March 31.

2. Confusing Financial Year with Calendar Year

India’s financial year is April 1 to March 31—not January to December. An investment on April 1, 2026, counts toward FY 2026-27, not 2025-26.

3. Not Collecting Receipts Immediately

Banks and fund houses sometimes don’t send confirmations automatically. Request them on the spot and keep digital copies via email.

4. Assuming Proposals Count as Investments

You submitted a PPF application on March 30, but the account opened on April 5. This won’t be deductible in FY 2025-26. Payment must be completed, not just proposed.

How to File Your Section 80C Investments in Your ITR

Once April comes and you’ve invested, here’s how to claim deductions:

- Download ITR-1 or ITR-2 from the Income Tax e-filing portal (incometaxindiaefile.gov.in)

- Fill Schedule 80C: List each investment with amount and date of investment

- Attach Supporting Documents: Upload scanned copies of receipts, certificates, and statements

- Verify with Your Bank/Employer: Ensure Form 16 (from employer) matches your investments

- File Before July 31, 2026 (extended deadline) or June 30 for earlier filing

If you’re unsure, use tax software like ClearTax, ET Money, or 1 India Tax, which guides you step-by-step. Alternatively, consult a Chartered Accountant like those recommended by the Indian Institute of Chartered Accountants (ICAI).

Final Checklist: Section 80C Investment Checklist March 2026

| Investment Type | Deadline | Max Limit | Status |

|---|---|---|---|

| PPF | March 31, EOD | ₹1.5 lakhs | ✓ Can still invest |

| Life Insurance Premium | March 31, EOD | Varies (within ₹1.5L 80C cap) | ✓ Can still pay |

| ELSS Mutual Funds | March 31, 3 PM | ₹1.5 lakhs | ✓ Can still buy |

| NSC | March 31, EOD | ₹1.5 lakhs (80C cap) | ✓ Can still buy |

| EPF (Voluntary) | March 31, EOD | ₹2.5 lakhs (₹1.5L 80C cap) | ✓ Can still contribute |

| Home Loan Principal | March 31, EOD | Amount actually paid | ✓ Can still pay extra |

Final Word: Act Now, Save Big

The Section 80C investment checklist is your roadmap to saving ₹30,000–₹60,000 in taxes before April 1, 2026. Whether you’re a 25-year-old freelancer earning ₹25 lakhs, a 40-year-old homemaker with investment income, or a 55-year-old planning retirement, these instruments fit every financial goal.

The key is action: calculate your remaining 80C limit today, choose 1-2 investments that align with your goals (PPF for safety, ELSS for growth, life insurance for protection), and complete payment before March 31. Delays of even one day push the deduction into the next financial year, costing you immediate tax relief.

Remember, tax-saving isn’t just about reducing taxes—it’s about redirecting that saved money into assets that grow over time. A ₹1 lakh PPF investment today becomes ₹2+ lakhs in 15 years. That’s how smart Section 80C investing transforms tax savings into wealth.

Don’t wait until April 1 to wonder, “What if I had invested more?” The deadline is March 31, 2026. Make your move today.