How to Maximize Tax-Saving FDs vs Regular FDs in May 2026: Complete Comparison for Conservative Investors

If you’re a salaried professional, retiree, or homemaker in India looking for safe, stable returns on your savings, you’ve likely heard of tax saving fixed deposits vs regular FDs India 2026. But what’s the real difference? And more importantly—which one should you choose?

Both options offer guaranteed returns without the volatility of stocks or mutual funds. Yet the tax implications, lock-in periods, and effective returns can vary dramatically. In May 2026, with interest rates stabilizing and new financial year planning underway, understanding these differences is critical.

This complete guide walks you through side-by-side comparisons, real rupee examples, and actionable strategies to help you decide which fixed deposit type maximizes your after-tax wealth.

Table of Contents

- What Are Tax-Saving FDs? Key Features Explained

- Regular Fixed Deposits: How They Work

- Tax-Saving FDs vs Regular FDs: Head-to-Head Comparison

- Real-World Calculation Examples for Indian Investors

- Who Should Invest in Tax-Saving FDs?

- Who Should Choose Regular FDs Instead?

- Step-by-Step Guide to Choosing the Right FD Type

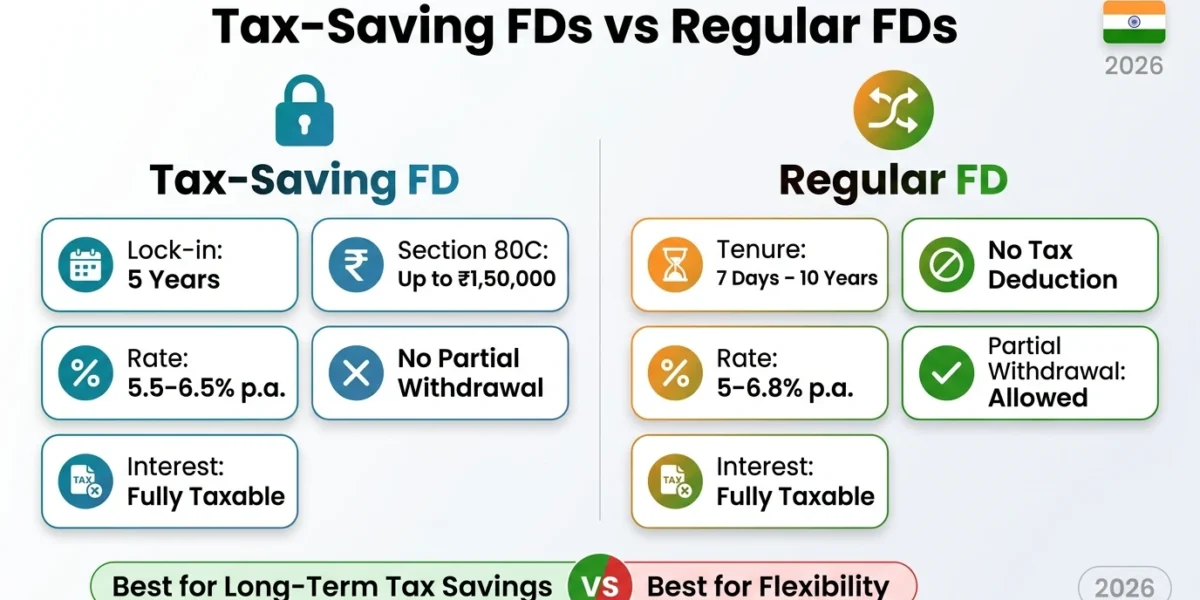

What Are Tax-Saving FDs? Key Features Explained

Tax-saving fixed deposits are special deposit schemes offered by banks that allow you to claim a deduction under Section 80C of the Income Tax Act. They’re designed specifically to help you reduce your taxable income while earning guaranteed returns.

Think of them as a double benefit: you get a safe return and a tax deduction in the same investment.

Core Features of Tax-Saving FDs:

- Mandatory 5-year lock-in period: You cannot withdraw your money before 5 years without losing tax benefits and paying a penalty.

- Section 80C deduction: You can claim up to ₹1,50,000 as a deduction in the financial year you invest. This directly reduces your taxable income.

- Interest rates: Typically 5.5% to 6.5% per annum (as of May 2026, depending on the bank).

- Compound interest: Interest is usually compounded quarterly or half-yearly.

- No partial withdrawals: Most banks don’t allow you to withdraw a portion before maturity.

- Tax on interest income: The interest you earn is taxable as per your income tax slab, even though the principal qualifies for Section 80C deduction.

Example: If you’re in the 30% tax slab and invest ₹1,50,000 in a tax-saving FD, you save ₹45,000 in taxes that year (30% of ₹1,50,000). That’s an immediate benefit—before the FD even matures.

Regular Fixed Deposits: How They Work

Regular fixed deposits are the traditional FDs most people know about. There’s no lock-in period, no tax deduction clause—just straightforward deposit, earn interest, withdraw anytime after maturity.

Core Features of Regular FDs:

- Flexible tenure: You choose from 7 days to 10 years (varies by bank).

- No tax deduction: The principal amount does not qualify for Section 80C or any tax deduction.

- Higher interest rates for longer tenures: Typically 5% to 6.2% per annum for 1-2 year deposits; 6% to 6.8% for 5+ year deposits.

- Partial withdrawal options: Many banks allow you to withdraw a portion (usually up to 50%) after a certain period, though it may incur a penalty.

- Flexibility on maturity: No forced lock-in—you can access your money whenever needed.

- Tax on interest income: All interest earned is fully taxable as per your income tax slab.

Example: Invest ₹1,50,000 in a regular 5-year FD at 6.5% per annum. At maturity, you’ll have approximately ₹1,97,000 (with quarterly compounding). The ₹47,000 interest is fully taxable.

Tax-Saving FDs vs Regular FDs: Head-to-Head Comparison

Here’s where the confusion usually starts. Both offer guaranteed returns, but they serve different financial goals. Let’s break down the comparison systematically.

| Feature | Tax-Saving FD | Regular FD |

|---|---|---|

| Lock-in Period | Mandatory 5 years | Flexible (7 days – 10 years) |

| Tax Deduction (Section 80C) | Yes, up to ₹1,50,000/year | No |

| Interest Rate (May 2026) | 5.5% – 6.5% p.a. | 5% – 6.8% p.a. |

| Partial Withdrawal | Not allowed | Allowed (with terms) |

| Interest Taxation | Fully taxable as per slab | Fully taxable as per slab |

| Best For | Long-term goals + tax savings | Flexibility + shorter goals |

The critical insight: Tax-saving FDs offer an upfront tax benefit, while regular FDs offer flexibility. Which matters more depends entirely on your financial situation.

Real-World Calculation Examples for Indian Investors

Let’s make this concrete with actual rupee numbers. We’ll compare the same investment amount under different tax slabs.

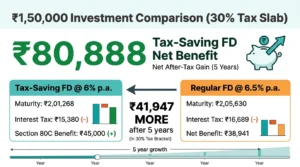

Scenario 1: Salaried Employee, 30% Tax Slab

Investment: ₹1,50,000 for 5 years

Tax-Saving FD at 6% p.a.:

- Maturity Value: ₹2,01,268 (with quarterly compounding)

- Interest Earned: ₹51,268

- Tax on Interest (30%): ₹15,380

- Tax Deduction Benefit in Year 1: ₹45,000 (30% of ₹1,50,000)

- Net After-Tax Gain: ₹51,268 – ₹15,380 + ₹45,000 = ₹80,888

Regular FD at 6.5% p.a.:

- Maturity Value: ₹2,05,630 (with quarterly compounding)

- Interest Earned: ₹55,630

- Tax on Interest (30%): ₹16,689

- Net After-Tax Gain: ₹55,630 – ₹16,689 = ₹38,941

Winner in 30% slab: Tax-Saving FD delivers ₹41,947 more net benefit over 5 years!

Scenario 2: Senior Citizen, 10% Tax Slab

Investment: ₹1,50,000 for 5 years

Tax-Saving FD at 6% p.a.:

- Maturity Value: ₹2,01,268

- Interest Earned: ₹51,268

- Tax on Interest (10%): ₹5,127

- Tax Deduction Benefit in Year 1: ₹15,000 (10% of ₹1,50,000)

- Net After-Tax Gain: ₹51,268 – ₹5,127 + ₹15,000 = ₹61,141

Regular FD at 6.5% p.a.:

- Maturity Value: ₹2,05,630

- Interest Earned: ₹55,630

- Tax on Interest (10%): ₹5,563

- Net After-Tax Gain: ₹55,630 – ₹5,563 = ₹50,067

Winner in 10% slab: Tax-Saving FD still wins by ₹11,074, but the gap is smaller.

This demonstrates a crucial principle: the higher your tax bracket, the more valuable the Section 80C deduction becomes. For high-income earners, tax-saving FDs are almost always superior.

Who Should Invest in Tax-Saving FDs?

Tax-saving FDs make sense if you match all or most of these criteria:

- You’re in the 20%, 30%, or higher tax slab: The tax deduction provides substantial immediate savings. If you’re in the 5% slab, the benefit shrinks dramatically.

- You have ₹1,50,000+ available annually to invest: To maximize the Section 80C deduction cap (₹1,50,000), you need that amount to invest. If you have less, a tax-saving FD might not be your best move.

- You don’t need the money for 5 years: The mandatory lock-in is strict. If you might need liquidity, avoid it.

- You have predictable income: Salaried employees benefit most because they know their tax bracket in advance.

- You want to combine tax deduction with investment: If you’re already investing in ELSS mutual funds or PPF (both Section 80C eligible), you can use tax-saving FDs to round out your allocation. Check our detailed 80C Tax Saving Investment Allocation Strategy 2026 High Income: ₹10L+ Earners guide for a complete 80C roadmap.

Who Should Choose Regular FDs Instead?

Regular fixed deposits are better if you fit these patterns:

- You’re in a low tax slab (5% or lower): The Section 80C benefit isn’t substantial enough to justify the 5-year lock-in.

- You need flexibility and liquidity: You might need your money in 2-3 years for a home renovation, wedding, or emergency. Regular FDs let you access funds with minimal penalty.

- You want shorter maturity periods: Some investors prefer 1-2 year FDs for better control and easier reinvestment decisions.

- You have unused Section 80C limit: If you’ve already maximized your 80C through PPF, ELSS, or life insurance, a regular FD doesn’t waste that space.

- You want higher interest rates: Banks sometimes offer slightly higher rates on longer-tenure regular FDs (5+ years) than on tax-saving FDs.

Step-by-Step Guide to Choosing the Right FD Type

Here’s a practical decision framework you can use right now:

Step 1: Calculate Your Annual Taxable Income

Check your last income tax return (or estimate if you’re new to filing). Know your tax slab: 5%, 20%, or 30%.

Step 2: Check Your Section 80C Utilization

Add up all investments you’ve already made under Section 80C in the current financial year:

- PPF contributions

- Life insurance premiums (LIC or private)

- ELSS mutual fund investments

- Home loan principal repayment

- Any other 80C-eligible investments

If the total is ₹1,50,000 or more, you’ve hit the cap—a tax-saving FD won’t add tax benefit.

If the total is less, calculate the gap. That gap is your available 80C space.

Step 3: Assess Your Liquidity Needs

Ask yourself honestly: Will I need this money in the next 5 years? Consider major life events: wedding, home purchase, child’s education, health emergency.

If yes—choose regular FDs with 1-3 year tenure.

If no—tax-saving FDs become viable.

Step 4: Compare Interest Rates Across Banks

As of May 2026, compare rates offered by major banks for both FD types:

- SBI

- HDFC Bank

- ICICI Bank

- Small Finance Banks (often offer 0.5-1% higher rates)

Even a 0.5% difference compounds significantly over 5 years.

Step 5: Calculate After-Tax Returns Using Your Slab

Use the formula below to compare:

For Tax-Saving FD:

Net Benefit = (Interest × (1 – Tax Rate)) + (Principal × Tax Rate)

For Regular FD:

Net Benefit = Interest × (1 – Tax Rate)

Compare the net benefit figures. The higher one is your winner.

Step 6: Make Your Decision and Invest

Once you’ve decided, open the FD through your bank’s online portal or visit a branch. Ensure you:

- Get the FD certificate via email/post

- Set a reminder for maturity date

- Plan reinvestment or withdrawal in advance

- If tax-saving FD, claim the deduction in your income tax return using the FD certificate

Final Thoughts: Tax-Saving FDs vs Regular FDs

Both tax-saving fixed deposits vs regular FDs India 2026 are safe, predictable investment vehicles. Neither carries market risk.

But they serve different purposes:

- Tax-saving FDs = Immediate tax savings + locked-in safety. Best for high-income earners with 5-year planning horizon.

- Regular FDs = Flexibility + no tax constraints. Best for those prioritizing liquidity or in lower tax brackets.

The ₹40,000-₹50,000 difference in after-tax returns (as shown in our examples) is substantial. Take the time to calculate your specific scenario before committing.

Remember: the best investment is the one aligned with your goals, tax situation, and liquidity needs—not just the one with the highest interest rate.